Opportunity cost is the most desirable alternative that someone gives up when they make a decision between two things.

Marginal cost is the amount it cost to add one more of something. The marginal benefit is the benefit of adding that one more of something.

Efficiency is using resources to their maximum ability to produce the most goods and/or services.

Growth is when the production possibilities curve moves to the right or the amount of goods that is being produced goes up.

Cost is the opportunity cost when one makes a decision.

The law of increasing cost is a principle that states when you shift from producing one thing to two, then more and more resources go into producing that second good or service. The opportunity cost increases.

A production possibilities curve is a graph that shows the different ways that an economy can use their resources. At a different point, it shows the different trade-offs that an economy has to make.

A production possibilities frontier is the line on the production possibilities curve that shows the maximum production for an economy.

- An example would be if you have $20 and go shopping for a video game. There are two games at the store that would fit your budget: War Zone 2 or Race Car Racing. Since you only have $20, you have to choose one or the other. If you pick up War Zone 2, then the opportunity cost to buy War Zone 2 was the chance to buy Race Car Racing.

Marginal cost is the amount it cost to add one more of something. The marginal benefit is the benefit of adding that one more of something.

- For example, if you had to make a decision in the morning to sleep-in in the morning or not, by having one more hour of sleep in the morning you would be well rested. By adding this one more, you are getting the benefit of being well rested (the marginal benefit).

Efficiency is using resources to their maximum ability to produce the most goods and/or services.

- For example, if you have land to grow apples and land to build factories on to make t-shirts, then you have to find the point in which all your resources are being used to their maximum benefit. Workers are considered a resource and so if you lay-off a hundred workers, then you have people that could be working that are not, so then the farms and factories would produce less items.

Growth is when the production possibilities curve moves to the right or the amount of goods that is being produced goes up.

- For example, if you have a set number of workers at a given time and all of a sudden their is a large wave of immigration then you have more resources. These resources can be put towards making more t-shirts and growing more apples so the economy sees some growth.

Cost is the opportunity cost when one makes a decision.

- If you have the land to grow apples on and build t-shirt factories, you should grow the apples on the land that is fertile and good for growing apples on. The factories will go on the other land. If you tear down the factory and started growing apple trees, since the land is not suitable for growing apples, then you are not using the land to the best ability. You have to make the decision to tear down the factory and grow the apples there.

The law of increasing cost is a principle that states when you shift from producing one thing to two, then more and more resources go into producing that second good or service. The opportunity cost increases.

A production possibilities curve is a graph that shows the different ways that an economy can use their resources. At a different point, it shows the different trade-offs that an economy has to make.

A production possibilities frontier is the line on the production possibilities curve that shows the maximum production for an economy.

|

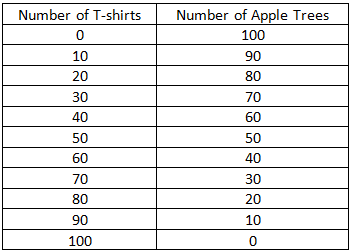

Looking at the table on the left, it shows the different production possibilities using the total resources in an area. if you wanted to make 40 T-shirts, then you would have 60 apple trees. Your decision to do this would be a trade-off. Trade-offs are necessary since there are only so many resources in an area.

|